Is a Carbon-Free World by 2050 a Guarantee or a Pipe Dream? An Analysis

Despite recent legislation, there is still considerable uncertainty around achieving net-zero emissions by 2050. Our best chance for reaching this goal is to support a plethora of climate technologies at various stages of maturity, including early adoption, demonstration, and prototype technologies. The barriers to adoption include cost and commercial risk, making government support a key factor in lowering costs and de-risking technologies.

Despite key legislation passed during the Biden Administration (i.e. Bipartisan Infrastructure Law, CHIPS and Science Act, and Inflation Reduction Act), it remains uncertain whether or not the United States and the world will reach net-zero targets by 2050.

The U.S. has dramatically increased funding for technologically-diverse clean energy projects, but what impact will this investment have? What technologies are being developed, and how will the legislation facilitate their commercial adoption?

Climate Technologies and Their Varying States of Maturity

Achieving net zero by 2050 will depend on the successful commercial deployment of a wide array of technologies at varying degrees of scientific and commercial maturity.

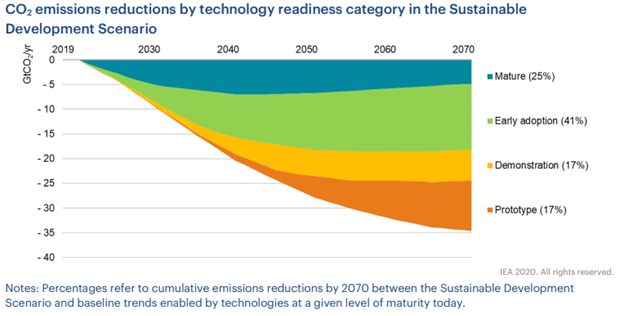

The International Energy Agency (IEA) has created four broad levels of technological maturity. Below are sample technologies that are within each category:

- Mature: hydropower, electric trains

- Early Adoption: offshore wind, onshore wind, solar energy, lithium-ion batteries, electric vehicles, heat pumps, low-greenhouse gas meat

- Demonstration: cement production with carbon capture, green hydrogen, long-duration energy storage, low-emissions plastics

- Prototype: steel production using hydrogen, direct air capture, advanced nuclear, enhanced geothermal energy, synthetic aviation fuels

To reach global net-zero emissions, all of these technologies must be commercially adopted at scale. In 2020, the IEA estimated that nearly 34% percent of the world’s emissions can only be abated by demonstration and lab-stage technologies. Furthermore, the IEA found that 41% of technologies that are critical for decarbonization are at an early adoption phase.

The largest barriers to commercial adoption of these technologies are cost and commercial risk: most consumers won’t pay more for comparable goods and services and most companies don’t want to invest in a factory type that has not been built before.

| Technology (sources cited) | Current Price Estimate | Target Price | Percent Premium |

| Electric Vehicles | $0.72 / mile driven | $0.63 / mile driven | ~14.3% |

| Clean Electricity | $0.15 / kWh | $0.13 / kWh | ~15.4% |

| Low Greenhouse Gas Meat | $5.04 – 5.76 / lb | $3.79 / lb | ~42.5% |

| Long-Duration Energy Storage | $1,100-1,400 / kW | $650 / kW | ~92.3% |

| Low-Emission Plastics | $1,087 – 1,155 / ton | $1,000 / ton | ~12.1% |

| Green Hydrogen Production | $3-6 / kg | $1 / kg | ~350% |

| Low-Carbon Cement | $219 – 300 / ton | $125 / ton | ~107.6% |

| Low-Carbon Steel | $871 – 964 / ton | $750 / ton | ~22.3% |

| Direct Air Capture | $250 – 600 / ton of CO2 abated | $100 / ton of CO2 abated | ~325% |

| Advanced Nuclear | $6,200 / kW | $3,600 / kW | ~72.2% |

| Sustainable Aviation Fuels | $5.36 – 8.8 / gallon | $2.22 / gallon | ~218.9% |

Governments have various levers to help lower cost and de-risk across the different levels of technological maturity.

Early Adoption Technologies

For “Early Adoption” level technologies, the greatest catalyst for mass adoption is subsidization of manufacturers, developers, and operators.

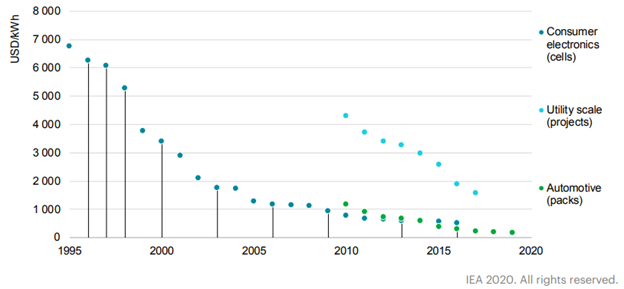

For example, electric vehicles and lithium-ion batteries, like solar panels before them, are experiencing a rapid cost reduction thanks, in part, to generous government subsidies. The science and product are mostly understood and optimized. The majority of remaining cost reductions can be achieved through learning by doing.

Now that the IRA has passed, this cost reduction is expected to accelerate. According to Bloomberg, the cumulative announced investment in electric vehicle manufacturing has increased from $13 billion to $52 billion in roughly five months.

Demonstration Technologies

For “Demonstration” level technologies, the greatest catalyst for cost reduction and commercial de-risking is public-private partnerships.

When the government partially funds and shares the risk of developing the first-of-a-kind industrial facility (say a clean hydrogen and energy storage facility), the technology and process can be proven to work on a commercial scale, and private investors will be much more likely to invest in future similar projects.

Furthermore, as companies partner with the government on innovation efforts, they can bring their expertise in scalability, reliability, and cost-effectiveness to catalyze the deployment of clean technologies. Avenues for engagement include partnering with National Laboratories, commercial and market data sharing, sponsoring research, and R&D tax credits. For example, Chevron’s partnership on demonstration projects has helped accelerate the oil major towards carbon capture, renewable natural gas, and green hydrogen technologies.

Prototype Technologies

For “Prototype” level technologies, the greatest catalyst for cost reduction is government funding of R&D.

From fundamental to applied science, these scientific and technological advancements drive lab spinouts and technology licensing.

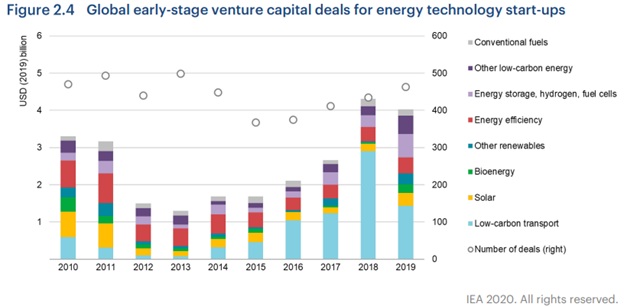

The recent increase in R&D spending starting from 2016 is also correlated with increased startup and venture capital investments in clean technology companies, as reported below.

Looking Forward

The data is clear that the world is not yet on track to reach net-zero emissions by 2050 considering how many essential technologies still lack commercial viability and scale. Recent legislation is moving the United States is moving in the right direction. However, we must remain vigilant as these laws roll out, learn from their results, and make prudent adjustments as needed.

This insight is a part of our Undergraduate Seminar Fellows’ Student Blog Series. Learn more about the Undergraduate Climate and Energy Seminar.

Derek He

2023 Kleinman Apollo FellowDerek He a second-year undergraduate in the Jerome Fisher Program in Management and Technology, studying computer science and business. He is the 2023 Kleinman Apollo Fellow and a 2023 Undergraduate Student Fellow.