IMF Links Low Interest Rates to Missing Stimulus from Oil Price Declines

Back in my February blog post, I explored a phenomenon baffling economists, low oil prices coupled with slow economic growth. Typically, low oil prices mean consumers spend less on energy and have more money in their pockets to spend on other things, creating economic stimulus. But this isn’t happening, and economists at the International Monetary Fund (IMF) have a theory as to why.

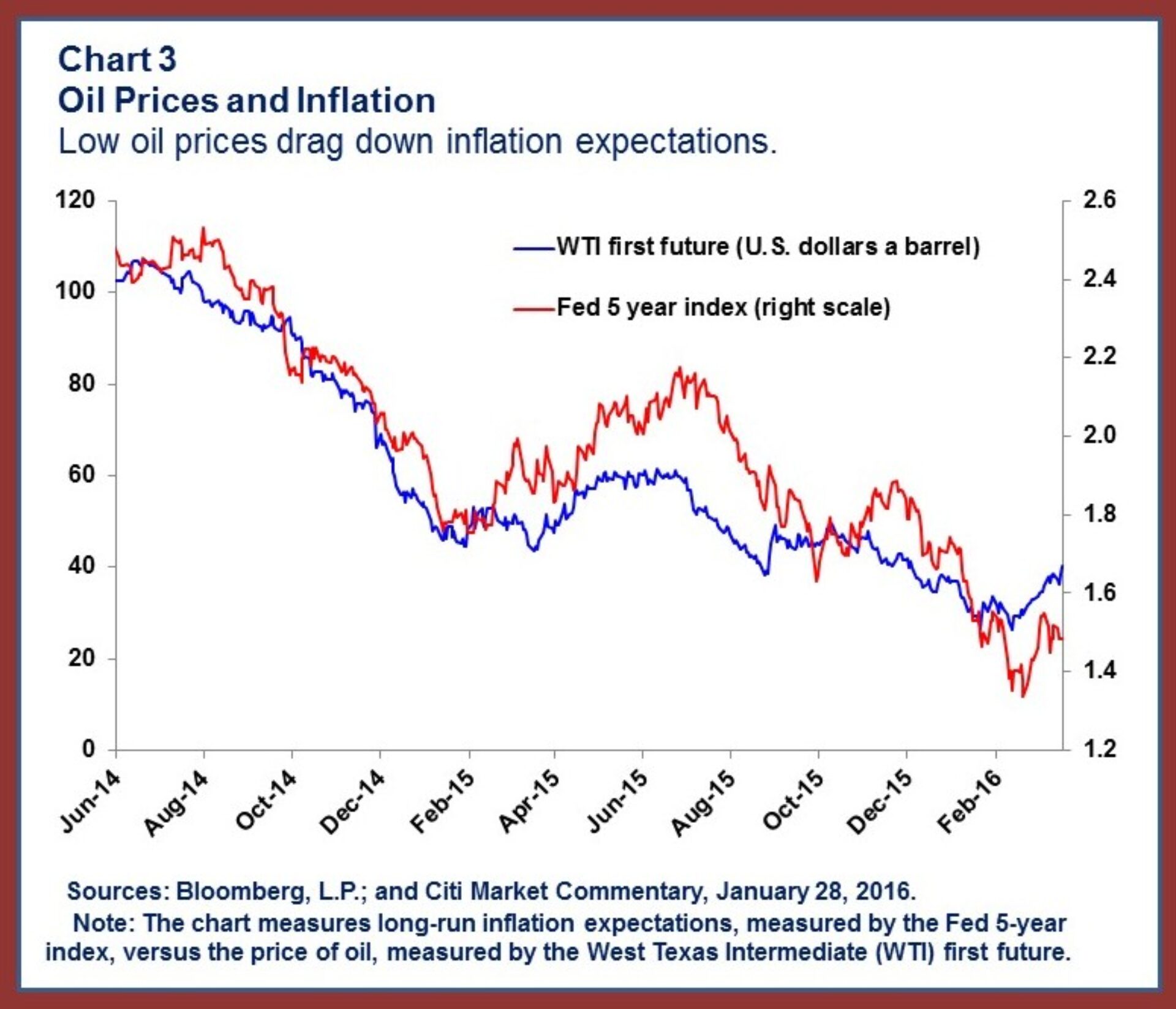

The IMF states that since June 2014, oil prices have dropped 65 percent (in U.S. dollar terms) as growth has progressively slowed in a wide range of countries. In addition, the IMF found that stock markets and oil prices are moving downwards together, rather than being countercyclical.

These trends have mystified many, including the IMF, all who expected low oil prices to support global growth as gains from net importers (mostly in developed countries where people are more active economic consumers) would eclipse losses from net exporters (typically in developing areas with lower economic consumption per capita).

The big difference this time is the low to zero interest rate environment that persists in many countries due to actions of central banks, according a blog preview of the IMF’s forthcoming 2016 World Economic Outlook.

First, the IMF indicates that low oil prices are due primarily to an oversupply of oil, followed by a softening in demand. Demand side reductions would lead to slowed growth tempered slightly by lower prices. The effect of high supplies – for example, from OPEC’s decision to continue production and new U.S. shale-based resources – coupled with low demand is pushing prices down further. Still, the mystery of the missing stimulus remains.

IMF attributes some of the missing growth to reduced capital investment as low oil prices make oil and gas ventures less attractive. They cite a $215 billion reduction in global capital expenditures in the oil and gas sector from 2014-2015, or about 0.3 percent of global GDP.

However, IMF believes a fundamental difference in this downturn cycle is that most central banks have no ability to lower interest rates to support growth, because interest rates are already so low.

The economists use stagflation (high inflation and low growth) from oil price increases as an example to show that when high oil prices increase costs to producers, the producers reduce output, layoff workers and increase the price of their products in order to combat the higher production costs. They argue the reverse should happen when oil prices drop; production and hiring should increase while product prices and inflation lower.

To understand the next part, one has to appreciate the relationship between inflation and interest rates. Inflation is a measure of how the price of goods and services are rising. As inflation increases, the same unit of money (e.g. a dollar) can purchase fewer goods. Central banks can change interest rates, for example if they are worried about inflation. Central banks establish and adjust interest rates, which impact the supply of money in an economy. Higher interests rates will make the cost of borrowing money more expensive and will decrease the supply of money available in the economy, and vice versa. If there is concern about too much inflation, central banks can increase interest rates to restrict credit and slow economic growth. If there is not enough growth (e.g. recession), central banks can lower interest rates to encourage borrowing and spur economic growth.

IMF indicates that in response to low growth from low oil prices and low inflation, a central bank might lower interest rates to spur growth, but that this is not possible given the rock-bottom rates that persist in many parts of the world. The economists argue that because nominal interest rates are near zero, declining inflation driven by reduced production costs (from low oil prices) results in a rise of the real rate of interest. For example, if the central bank’s nominal interest rate is 0 percent and the rate of inflation drops from 4 percent to 2 percent, the real interest rate has risen from -4 percent to -2 percent.

IMF believes this rise in the real rate of interest may be reducing demand and preventing increases in output and employment that would otherwise happen when production input costs decrease. They go on to identify the unexpected outcome of rising oil prices potentially unleashing economic growth as real interest rates decline in the absence of central bank rate increases.

The economist’s full analysis will be available in the 2016 World Economic Outlook, due to be released in April.

Christina Simeone

Kleinman Center Senior FellowChristina Simeone is a senior fellow at the Kleinman Center for Energy Policy and a doctoral student in advanced energy systems at the Colorado School of Mines and the National Renewable Energy Laboratory, a joint program.