Policy Design Issues for Border Carbon Adjustments

Border carbon adjustments (BCAs) are an increasingly popular climate policy tool, with the European Union's Carbon Border Adjustment Mechanism set to take full effect in 2026. This brief explores the complex policy design issues entailed in BCAs, and how to make them work.

At A Glance

Key Challenge

In principle, BCAs can help ensure that a country with a high carbon price doesn’t disadvantage domestic producers, but they are complex and difficult to implement and administer.

Policy Insight

Creating a platform to share lessons learned from the world’s operational BCAs can promote policy learning and best practices for other countries considering developing similar measures.

Introduction

Setting a price on greenhouse gases, especially carbon dioxide, is widely understood to be a critical component of policy measures to address climate change (Siriwardana, Meng, and McNeill 2017; Dominioni and Esty 2023). However, in the absence of a global carbon price, the setting of such prices in individual countries creates a risk that emissions-generating economic activity will simply move to a jurisdiction with lower or no emissions pricing.

This risk, known as carbon leakage, is not only environmentally damaging but economically and politically harmful as well, since it implies harm to domestic producers and may deter political leaders from pursuing emissions pricing in the first place (Dolphin and Ferrucci 2025).

One solution to the problem of leakage is the Border Carbon Adjustment (BCA), which aims to equalize the carbon price paid by foreign and domestic producers of emissions-intensive goods (Dominioni and Esty 2023; Condon and Ignaciuk 2013).

In principle, this parity prevents foreign producers from gaining an advantage over domestic competitors subject to emissions pricing. In practice, however, designing BCAs involves a series of exceptionally complex policy design considerations.

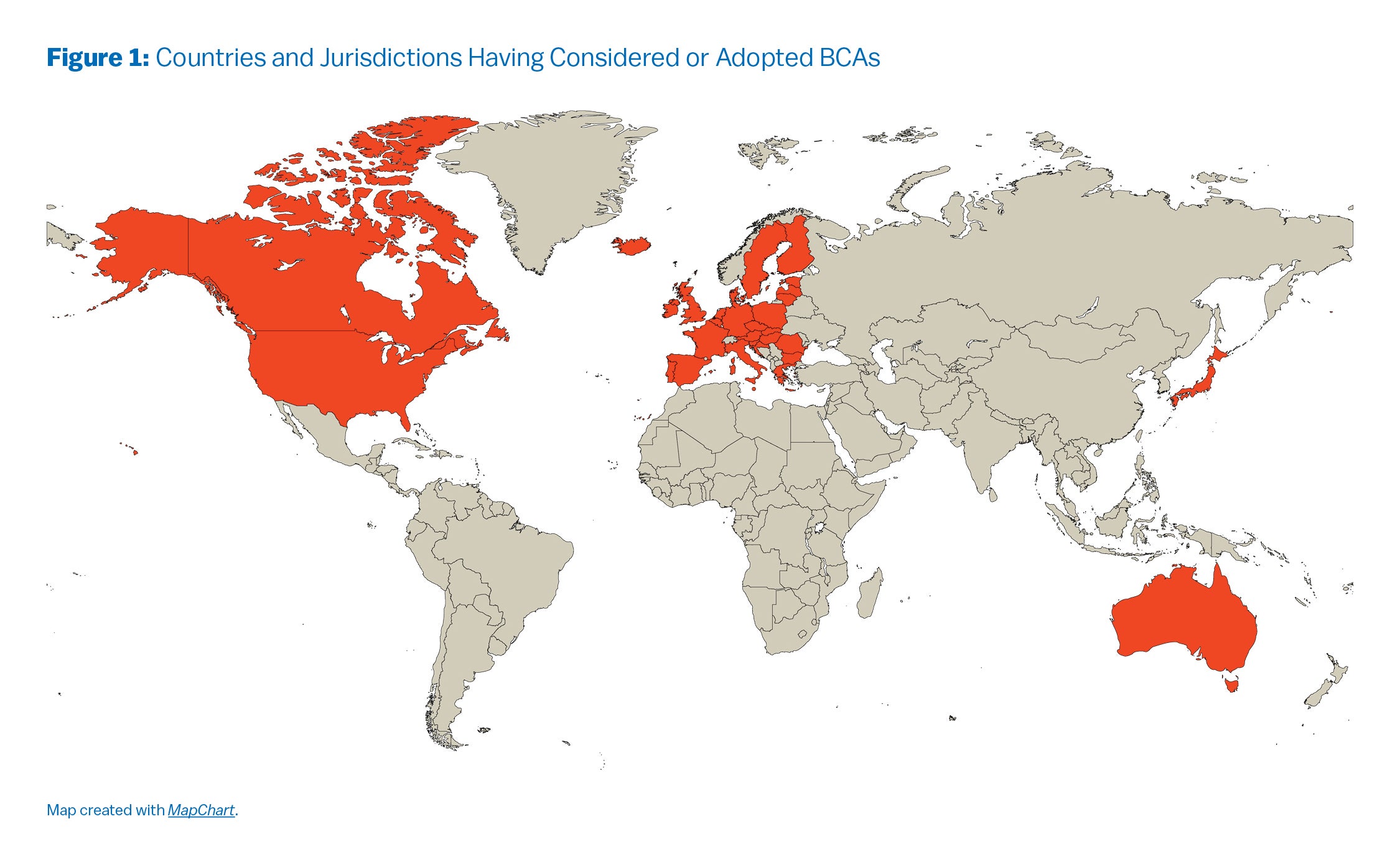

This issue brief identifies these considerations drawing on extent and proposed BCAs. The European Union (EU) has a BCA known as the Carbon Border Adjustment Mechanism (EU CBAM) that will begin full operation in January 2026, while the United Kingdom will institute one in 2027.

In addition, the governments of the United States, Canada, Australia, and Japan have also formally proposed or studied BCAs (see Figure 1). Not all of these proposed BCAs are purely economic in nature: the U.S. proposals, for example, would take the place of an economy-wide carbon price, and are at least partly geopolitical in objective.

With this diversity of objectives in mind, a core concern of this analysis is the extent to which BCAs can represent a subject of productive dialogue and advance diplomatic, economic, and climate cooperation between major economies. Much of what is known about the function of BCAs stems from the EU CBAM, the world’s largest and most prominent BCA. Accordingly, the next section examines the EU CBAM.

Structure of the EU CBAM

The EU CBAM is designed to reduce carbon leakage as a result of the EU’s Emissions Trading System (ETS), especially as the price of emission permits increases and free allowances are phased out in accordance with the EU’s Green New Deal (Dolphin and Ferrucci 2025). As a policy, CBAM obliges importers of certain goods into the EU to purchase certificates corresponding to the quantity carbon dioxide emissions embedded in imported goods. Importers must also calculate and report these emissions.

The CBAM covers both direct emissions for a set of goods that currently include aluminum, iron and steel, cement, fertilizer, and hydrogen goods, as well as indirect emissions from electricity use for cement and fertilizer production. These goods were chosen because of their highly carbon-intensive nature as well as vulnerability to carbon leakage (Dolphin and Ferrucci 2025).

The price of certificates is, at the time of writing, benchmarked to the EU ETS at 100 USD per metric ton of carbon dioxide. Importers began having to report their emissions in 2023, and will be required to purchase certificates beginning in 2026 (European Commission 2024a, 2024b).

Perhaps the most complex part of the CBAM involves the calculation of embedded emissions. The CBAM regulation requires importers to report the quantity of goods imported and their Combined Nomenclature (CN) codes along with countries and specific installations where the goods were produced as well as details on the technologies and the emissions factor for electricity used to produce these goods.

In addition, for certain products, importers must also report electricity consumption involved in the production process for these goods. Up to 20% of the intensity of the total embedded emissions may be calculated using estimates rather than direct measurements. A penalty is authorized for each ton of unreported emissions (European Commission 2024b).

These provisions entail very significant measurement obligations at nearly any facility that produces goods subject to the CBAM and that may be imported into the EU. The actual calculation of fees due is benchmarked to carbon prices under the EU ETS and includes a discount for any carbon prices paid on the goods in other countries.

Other Proposed BCAs

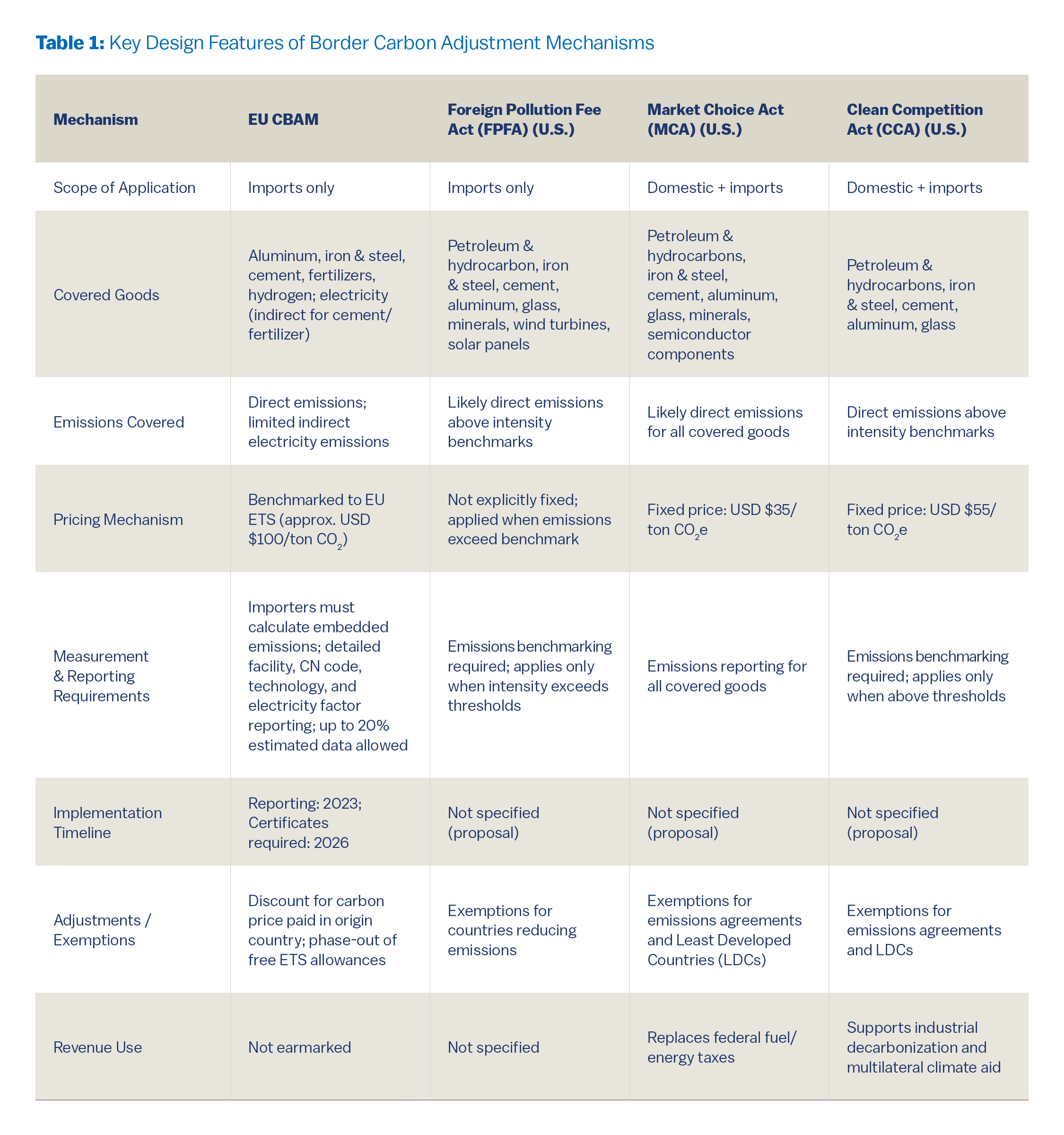

Apart from the EU CBAM, various forms of BCAs have been proposed or formally studied by governments in at least five other jurisdictions: the United States, Canada, the United Kingdom, Japan, and Australia. In the United States, at least four pieces of legislation have been introduced in Congress that include BCA-related provisions. Three of these proposed bills, the Foreign Pollution Fee Act (FPFA), the Market Choice Act (MCA), and the Clean Competition Act (CCA), would create BCA mechanisms.

Table 1 summarizes key features of these provisions in comparison to the EU CBAM. The three bills differ in coverage, with both the MCA and CCA applying to both domestic and imported goods while the FPFA applies only to imported goods. The bills also encompass different products. While all three include petroleum and hydrocarbon products, iron and steel, cement, aluminum, and glass, the FPFA and MCA also include minerals.

The FPFA further includes wind turbines and solar panels, while the MCA includes semiconductor components. The FPFA and CCA are structured to apply only to products whose emissions intensity exceeds certain benchmarks, while the MCA applies to all covered products. The CCA and MCA both set specific carbon prices of USD$55/ton of carbon dioxide equivalent (CO2e) and USD$35/ton of CO2e, respectively.

The CCA also directs that revenue raised from the BCA be directed to supporting decarbonization in affected industries as well as towards multilateral climate assistance, while the MCA would replace federal gasoline and other energy taxes. Notably, all three bills also include exceptions for countries that enter into agreements to reduce emissions or, in the case of the CCA and MCA, are among the least developed countries (Gangotra, Carlsen, and Kennedy 2023).

In October 2024, the United Kingdom (UK) government committed to instituting its own CBAM beginning in January 2027. The design of the UK CBAM is broadly similar to that of the EU, though it is benchmarked to the UK rather than EU ETS, and at the time of writing it is intended to cover both direct and indirect embodied emissions for all covered products as opposed to only a selection as is the case with the EU CBAM (HM Treasury 2025). In 2020, the Government of Canada announced that it would consult with like-minded countries on BCAs, though there is little sign of subsequent action (Department of Finance Canada 2025).

In 2023, the Australian Government announced that it would undertake a review of carbon leakage, part of which would include an assessment of the feasibility of an Australian CBAM, especially in relation to steel and cement. At the time of writing, two rounds of public consultation had been completed (Department of Climate Change, Energy, the Environment, and Water 2025). Finally, the Japanese Government formally studied CBAMs, but has so far stopped short of endorsing the implementation of a domestic BCA (Ministry of Economy, Trade, and Industry (Japan) 2022).

Outstanding Issues and Concerns

Despite the growing global popularity of BCAs and the implementation of the EU CBAM, there are several major questions surrounding their use that remain unresolved. The first and perhaps most foundational of these relates to its legality under World Trade Organization (WTO) law.

This law stipulates that WTO members must generally not discriminate between exporting countries and not apply charges to imported goods that differ from those applied to equivalent domestic products. However, WTO rules generally pertain to physical traded goods such as commodities, rather than energy inputs or outputs in the form of emissions. In addition, trade law contains exceptions for mechanisms “necessary to protect human, animal or plant life or health,” which some scholars argue pertains to climate change (Dominioni and Esty 2023).

A related concern is the impact of BCAs on developing countries. Major developing economies generally oppose BCAs on principle, either in relation to the nondiscrimination provisions of WTO law or common but differentiated responsibility (CBDR) under the United Nations Framework Convention on Climate Change (UNFCCC) (Dev and Goswami 2024); (Chen et al. 2025).

Notably, Chinese government representatives have expressed strident opposition to BCAs in general and the EU CBAM in particular, which they have characterized as a “carbon tariff” in violation of WTO rules and the principle of CBDR (Pang 2023). A 2021 meeting of BRICS (Brazil, Russia, India, China,

and South Africa) Environment Ministers moreover criticized BCAs as “discriminatory unilateral trade barriers” (Zhang 2023).

The burden of compliance with EU CBAM reporting requirements is also frequently criticized by developing country exporters. In a consultation convened by the International Institute for Sustainable Development, for example, South American exporters noted that much of the information required by EU CBAM reporting requirements is not easily available and would require significant, expensive investments in measurement and data collection (Bonnet 2024).

A further outstanding question relates to the potential for BCAs to reduce emissions, especially in China, the world’s largest national source of greenhouse gas emissions. China is estimated to account for 15% of the total volume of commodities trade exposed to the EU CBAM, among the highest of any single country.

Given the relatively limited list of goods currently covered by the EU CBAM, the estimated impact both on the Chinese economy and on China’s emissions is expected to be limited, to a few hundred million dollars and a few million tons of carbon dioxide, respectively (Chen et al. 2025).

It is possible however that the CBAM will drive significant emissions reductions in exposed industries. For example, a Chinese-language article suggests that in part because of the EU CBAM, technological upgrades may reduce the emissions intensity of Chinese steel production from approximately 0.6 kg of carbon dioxide per ton to 0.45 (Zhang 2023).

The case of China also points to outstanding questions related to the role of BCAs in advancing or limiting international climate cooperation. The U.S. FPFA is explicitly motivated by geopolitical as well as economic and environmental objectives, namely to reduce the reliance of American industries on China-centric supply chains (Moore 2025).

The fact that BCAs are most popular among traditionally close Western allies further lends them a geopolitical dimension and the implication that they are a function of competitive rather than cooperative dynamics in international relations (Francis, Hoenig, and Rooper 2023); (Moore 2025). Yet BCAs are not inherently at odds with international climate cooperation, especially between major economies.

Indeed, it is worth noting that China itself, with the world’s largest ETS by volume, may well benefit from instituting some form of BCA in the future, particularly if its own labor and other costs rise to the point that lower-cost producers emerge for emissions-intensive industries like steel and cement manufacture. Accordingly, the next section turns to opportunities for diplomatic engagement and cooperation on BCA policy design.

Opportunities for Partnership

BCAs are an important solution to the problem of carbon leakage, and in many ways serve as a necessary adjunct to better-known and better-understood carbon pricing instruments. However, as the foregoing analysis has demonstrated, they are exceptionally complex to develop and administer. Moreover, BCAs implicate important international legal and ethical questions and are diplomatically controversial.

These features lend BCAs important political as well as economic and environmental aspects. However, they also create an opportunity for shared policy learning and dialogue between jurisdictions seeking to implement BCAs. At least three features of BCAs stand out as opportunities for such learning and dialogue:

- Reducing administrative complexity and compliance costs: adopting uniform standards for emissions reporting and verification would reduce complexity between jurisdictions seeking to implement BCAs, as well as reduce compliance costs for affected industries. However, realizing these benefits would require jurisdictions to develop and agree to utilize common standards for emissions intensity and reporting. Given that the EU CBAM will be the first large-scale BCA to enter into force, it makes sense to adopt CBAM standards.

- Explore multilateral benefit sharing: a frequently-proposed refinement to BCA policy design, including in stakeholder consultations, is to allocate some of the revenue raised to support decarbonization or climate-related assistance in developing countries (Bonnet 2024). Doing so would at least in principle address the objection from developing countries that BCAs impose unfair and disproportionate burdens on their economies.

- Pursue joint BCA diplomacy: as this report has suggested, important questions remain concerning the applicability of international trade rules as well as the principle of CBDR to BCAs. Jurisdictions seeking to implement BCAs would benefit from pursuing joint diplomatic engagement, including within the WTO and UNFCCC, to address these questions as well as potential opposition from developing countries.

Each of these questions could be addressed as workstreams under a dedicated International BCA Policy Forum or similar intergovernmental entity. This entity would bring together jurisdictions either having already implemented or exploring the use of BCAs to facilitate joint policy learning and reform.

It could seek observer or consultative status with related entities such as the WTO and UNFCCC to support integration with other relevant international policy dialogues. Such a platform would likely be an important means of helping jurisdictions both successfully implement complex BCA policy designs while also addressing some of the thorny diplomatic issues involved in their implementation at scale.

BCAs have enjoyed significant popularity in recent years as a component of climate and energy policy in several major economies. While it remains unclear if jurisdictions like Canada and Australia that have considered BCAs in the past will move toward implementation, it is worth noting that BCAs offer policymakers an option to advance both climate policy goals while also appealing to domestic industries and constituencies concerned about employment disruption and competitiveness impacts due to emissions pricing. As the world continues to face intense pressure to reduce emissions, BCAs will remain an important policy tool, and one for which continued dialogue and cooperation will be essential to developing as efficiently and effectively as possible.

Scott Moore

Managing Director, Penn GlobalScott Moore is a faculty fellow at the Kleinman Center for Energy Policy and Managing Director of Global Initiatives, Research, and Strategy. He is also a practice professor of political science.

Bonnet, Antoine. 2024. “Global Dialogue on Border Carbon Adjustments: Stakeholders’ Perspectives in Brazil, Canada, Trinidad and Tobago, the United Kingdom, and Vietnam.” International Institute for Sustainable Development.

Chen, Zhe-Yi, Lu-Tao Zhao, Lei Cheng, and Rui-Xiang Qiu. 2025. “How Does China Respond to the Carbon Border Adjustment Mechanism? An Approach of Global Trade Analysis.” Energy Policy 198 (March): 114486. https://doi.org/10.1016/j.enpol.2024.114486.

Condon, Madison, and Ada Ignaciuk. 2013. Border Carbon Adjustment and International Trade. OECD Trade and Environment Working Papers. https://doi.org/10.1787/5k3xn25b386c-en.

Department of Climate Change, Energy, the Environment, and Water. 2025. “Australia’s Carbon Leakage Review.” Reducing Emissions. February 19, 2025. https://www.dcceew.gov.au/climate-change/emissions-reduction/review-carbon-leakage.

Department of Finance Canada. 2025. “Exploring Border Carbon Adjustments for Canada.” Consultations. January 14, 2025. https://www.canada.ca/en/department-finance/programs/consultations/2021/border-carbon-adjustments/exploring-border-carbon-adjustments-canada.html.

Dev, Trishant, and Avantika Goswami. 2024. “China and the CBAM.” Edited by Souparno Banerjee. The Global South’s Response to a Changing Trade Regime in the Era of Climate Change. Center for Science and Environment.

Dolphin, Geoffroy, and Gianluigi Ferrucci. 2025. “The EU’s CBAM.” IMF Working Papers 2025 (125): 1. https://doi.org/10.5089/9798229000420.001.

Dominioni, Goran, and Daniel Esty. 2023. “Designing Effective Border Carbon Adjustment Mechanisms: Aligning the Global Trade and Climate Change Regimes.” Arizona Law Review 61 (1): 2–40.

European Commission. 2024a. “CBAM Guidance and Legislation – Taxation and Customs Union.” CBAM Guidance and Legislation. May 30, 2024. https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism/cbam-guidance-and-legislation_en.

———. 2024b. “Implementing Regulation – 2023/1773 – EN – EUR-Lex.” Commission Implementing Regulation (EU) 2023/1773 of 17 August 2023 Laying down the Rules for the Application of Regulation (EU) 2023/956 of the European Parliament and of the Council as Regards Reporting Obligations for the Purposes of the Carbon Border Adjustment Mechanism during the Transitional Period (Text with EEA Relevance). October 31, 2024. https://eur-lex.europa.eu/eli/reg_impl/2023/1773/oj/eng.

Francis, Reuben, Daniel Hoenig, and Holly Rooper. 2023. “Getting Ahead of the Curve: Primer on Border Carbon Adjustment Policy Proposals.” Climate Leadership Council.

Gangotra, Ankita, Wily Carlsen, and Kevin Kennedy. 2023. “4 U.S. Congress Bills Related to Carbon Border Adjustments in 2023.” Project Update. World Resources Institute.

HM Treasury. 2025. “Factsheet: Carbon Border Adjustment Mechanism .” Gov.Uk. April 24, 2025. https://www.gov.uk/government/publications/factsheet-carbon-border-adjustment-mechanism-cbam/factsheet-carbon-border-adjustment-mechanism.

Ministry of Economy, Trade, and Industry (Japan). 2022. “Trade and the Environment: An Overview of the Carbon Border Adjustment Mechanism and Compatibility with WTO Rules.” Report on Compliance by Major Trading Partners with Trade Agreements. Ministry of Economy, Trade, and Industry (Japan).

Moore, Scott M. 2025. “Carbon Tariffs: The Future of Climate Policy.” Perry World House. January 22, 2025. https://perryworldhouse.upenn.edu/news-and-insight/carbon-tariffs-the-future-of-climate-policy/.

Pang, Wuji. 2023. “欧盟‘碳关税’COP28期间受到包括中国在内多国批评 [EU ‘CBAM’ Critized by Several Countries Including China at COP28].” Sina News. August 12, 2023. https://news.sina.cn/sx/2023-08-09/detail-imzfqfae1116491.d.html?utm_source=chatgpt.com.

Siriwardana, Mahinda, Sam Meng, and Judith McNeill. 2017. “Border Adjustments under Unilateral Carbon Pricing: The Case of Australian Carbon Tax.” Journal of Economic Structures 6 (1): 34. https://doi.org/10.1186/s40008-017-0091-x.

Zhang, Wenbin. 2023. “中国钢铁业碳中和应对欧盟CBAM外部市场挑战 [China’s Carbon Neutral Steel Industry Responds to the External Challenges of EU CBAM].” Sina News. August 9, 2023. https://news.sina.cn/sx/2023-08-09/detail-imzfqfae1116491.d.html?utm_source=chatgpt.com.